57.2 Risk Preference Function

TreeAge Pro is able to record your risk function as a mathematical curve and apply this curve to the expected value of an uncertainty. Recommendations are then made based on your derived certainty equivalents, rather than on expected values.

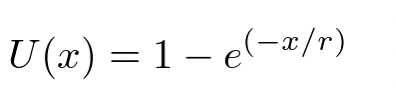

There are two types of curves, or risk functions, which TreeAge Pro can use. The constant risk aversion function is calculated using the formula:

where U is an arbitrary utility scale, and r is a risk preference coefficient, described below. The utility scale is used only for internal calculations; the formula’s inverse is later applied to find certainty equivalents.

The non-constant risk function is tailored to fit your specific model, and so is superior to the constant risk aversion function in many respects, except that it takes a little longer to set up initially. TreeAge Pro will ask you a series of questions about your certainty equivalents for the model you are working on. It will then create a curve made up of line segments approximating your true risk function.

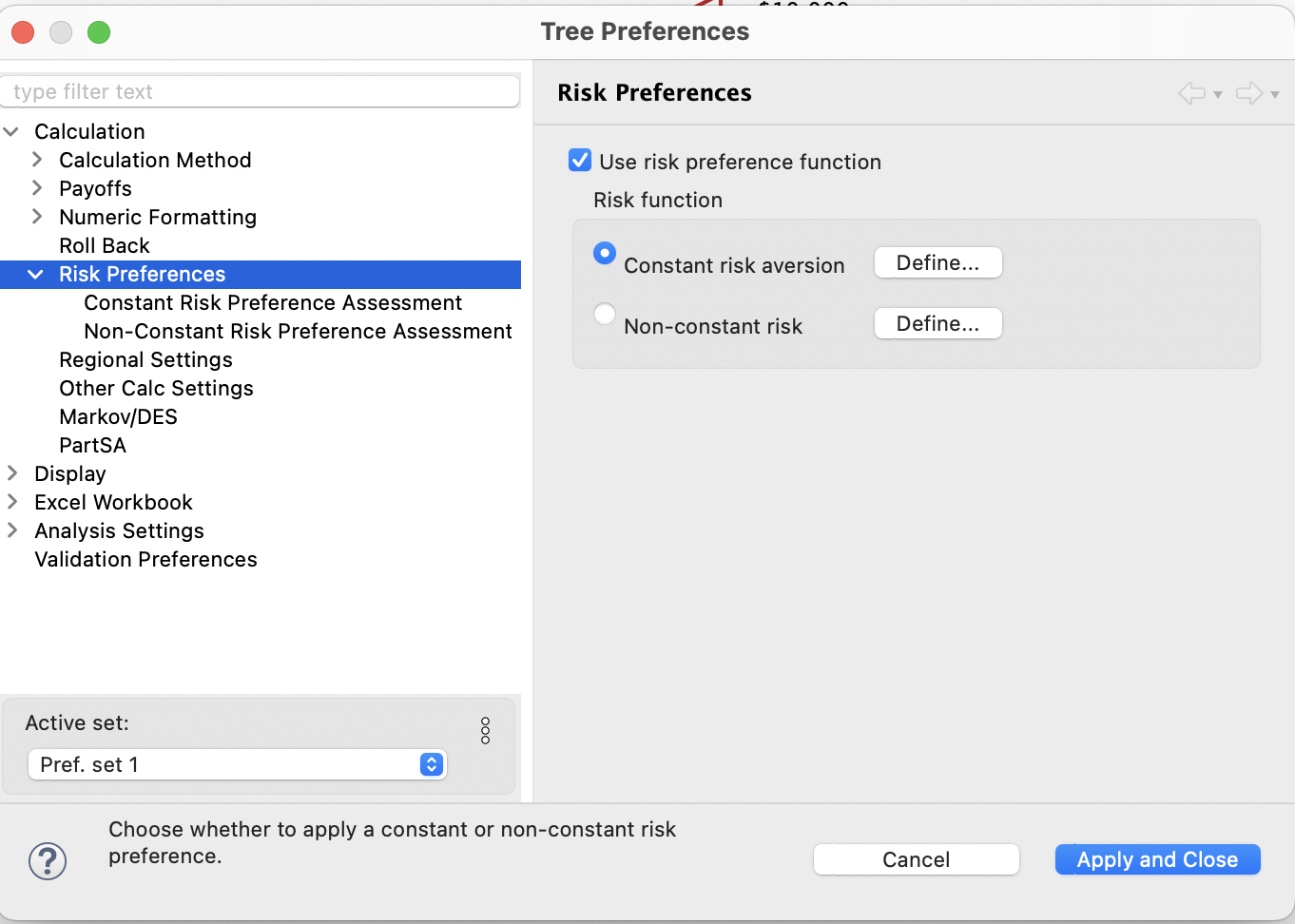

Both types of risk functions are entered via Tree Preferences.

To use risk preferences when analyzing a model, check the Use risk preference function box and select either Constant risk aversion or Non-constant risk.

57.2.1 Constant risk aversion

If constant risk aversion is selected, you will be asked to supply a single value. Specifically, you will be shown a generic lottery in which you have a 0.5 probability of winning X and a 0.5 probability of losing one-half X, and asked to specify the largest value of X for which you would be willing to take part in the lottery. This value is used as the risk preference coefficient in the above formula.

The lottery might represent an investment in a biotech company which is about to get a judicial ruling on the validity of an important patent. If the ruling is favorable (0.5 probability), the investment will double in value; if unfavorable (0.5 probability), the investment will fall in value by 50%.

What is the most you would invest under these circumstances? This amount is referred to as your risk preference coefficient.

57.2.2 Non-constant risk aversion

Non-constant risk aversion allows you to enter utilities (value to you) for different values in the model. These utilities are used to create a non-constant risk function that is applied to your model.